Evidence is beginning to develop that, despite the seriousness of the recession; household balance sheets can be stabilized, particularly as the employment picture improves in coming years. Improving household financial conditions will be vital to initiating and sustaining an economic recovery and stabilizing consumer spending, particularly on housing.

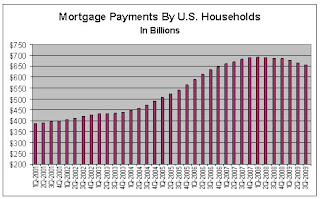

Initial evidence of initial improvement can be seen in the total mortgage obligations of American households. Total mortgage payments by U.S. households, from the Bureau of Economic Analysis are shown below.

The aggregate payments shown above can be reduced by a number of factors including the lowering of weighted interest rates which has occurred in recent months. Foreclosure, whether caused by loss of employment or by strategic choice, will also act to reduce the outstanding loan balances over time. Selling a vacation home, a short sale or forced foreclosure all act to reduce the aggregate payments made by households. Given the amount of time it is currently taking to process a foreclosure, the decline in payments data is clearly a lagging indicator and acceleration in the decline in payments is presumably already taking place.

Even if a new mortgage is originated from the sale of a foreclosed unit the loan balances is likely to be far lower than the balance of the previous owner, particularly when previous junior liens are considered. Thus the payments picture is likely to improve even as distressed inventory is absorbed.

Magnifying the improving trend in payments is data from the multi-family sector that suggests many senior citizens, college students and “boomerang” young adults are returning to the primary household to economize. This suggests an increasing ability, over time, of households to maintain at least one “core” family residence, family-owned or not.

The elimination of an oversized house payment from the household budget or an increase in the household income generated by adding additional income sources have the potential to rehabilitate a household balance sheet. A more challenging proposition will likely be convincing the family that buying a home in the future will present a “good” investment and viable financial step.

John Mulville

Real Estate Economics

http://www.realestateeconomics.com